A stablecoin is a type of cryptocurrency designed to be linked to the price of a specific asset, such as legal tender or commodities.

In this article, we will explain in detail the characteristics and types of stable coins, which are attracting attention as a new means of payment utilizing P2P (Peer to Peer) characteristics, as well as trends in regulations in abroad.

What is Stablecoins?

Stablecoin is a type of cryptographic asset designed to be linked to the price of a specific asset, such as a legal tender such as the US dollar or a commodity. Conventional cryptocurrency such as Bitcoin and Ethereum have large price fluctuations (volatility), and although they have functions that legal tender does not have, they lack practicality and stability as a means of payment.

If a stablecoin is linked to legal tender, it will have the same value as legal tender even though it is a cryptocurrency. With the creation of stablecoins, cryptocurrencies can remain stable in value.

Growth of the Stable Coin Market

The history of cryptocurrency began with the creation of Bitcoin in 2009, but it is only in the last few years that stablecoins have come into serious use.

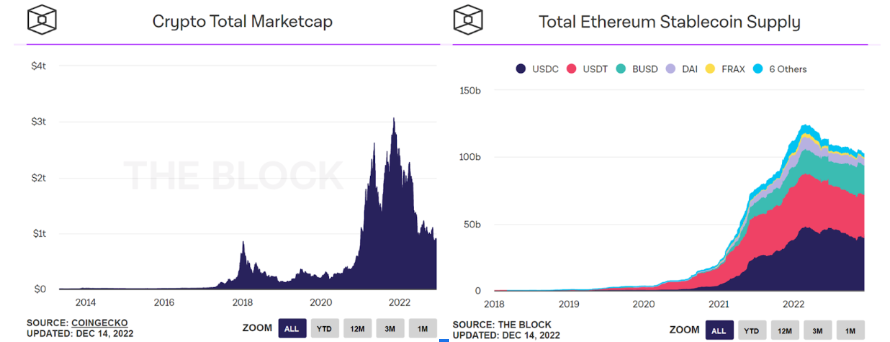

In early 2020, the market capitalization of the stable coin market was less than $7.3 billion. However, as of December 2022, it exceeded $146 billion, indicating that the stable coin market has been developing rapidly.

The year 2022 was a year of significant cooling in the cryptocurrency market, with industry insiders whispering of a “cryptowinter” (winter period). The total market value of cryptocurrency has fallen below $1 trillion, less than 1/3 of the peak in 2021, and cryptocurrency trading volume has also declined significantly.

On the other hand, the situation is different for the stable coin market. The following chart compares the total market capitalization of cryptocurrencies and the total supply of stable coins. While the total market capitalization of cryptocurrency has declined significantly to less than 1/3 of its peak in 2021, the total supply of stable coins has not declined much since its peak and has remained high.

Citation: THE BLOCK

Even in a weak market environment, there is not that much demand for stablecoin redemption, and it is assumed that funds are staying in the cryptocurrency market.

This is likely due to the expansion of use cases for stablecoins. A prime example is the rise of DeFi (decentralized finance ) services. Users can earn fees and interest income by depositing funds into DeFi services such as liquidity mining and yield farming. Such DeFi operations are also possible with stable coins, which may provide an incentive to hold stable coins.

In addition, use cases by businesses are expected to expand in the future. Recently, USDC is now available for Apple pay, and FV Bank, a bank in the Autonomous Community of Puerto Rico, has announced that it will support USDC customer deposits. Until now, cryptocurrency has had many use cases as speculative assets, but as more and more use cases are linked to real life, such as payment methods and bank deposits, the incentive to hold stablecoins is expected to increase further.

Why Stablecoin is important

So far we have discussed the rapid growth of the stable coin market. So why are stablecoins considered an important asset?

In a nutshell, this is because stablecoin is an asset that combines the strengths of blockchain that legal tender does not have, while being unaffected by the volatility of cryptocurrency.

cryptocurrency are volatile and change in value frequently. When market uncertainty increases, there is a demand to “exchange for safe assets” to reduce the risk of price fluctuations, but before the birth of stablecoin, the only way to do this was to sell cryptocurrency for legal tender. Since conversion to legal tender could only be done on an exchange, it was also necessary to transfer cryptocurrency held on the exchange.

After the birth of stablecoin, the value can be stabilized as a cryptocurrency. The exchange of cryptocurrency into stablecoin is also possible through AMM (Automated Market Maker) based services, so a transfer to an exchange is not always necessary.

Another strength of stablecoin is that it inherits the properties of a cryptographic asset. Unlike legal tender, stablecoin is a token issued on the blockchain, allowing for peer-to-peer(P2P) transfers. This means that money can be transferred instantly with low fees.

This is not due to the characteristics of stablecoin itself, but it has also played a role in increasing market liquidity as stablecoin has come to be used as the key currency for cryptocurrency trading. Exchanges are now able to improve the liquidity of certain cryptocurrency by offering stable pairs

Types of Stable Coins

From this point forward, the types of stable coins will be explained.

There are many types of stable coins, but they can be classified into four main categories based on the different mechanisms that stabilize their value.

- legal tender-backed

- Crypto asset-backed

- Algorithm type (unsecured)

- commodity type

Legal tender-backed

Legal tender-backed stablecoins are, as the name suggests, backed by legal tender such as the U.S. dollar.

The following are representative legal tender-backed stablecoins. All of these stablecoins are linked to the U.S. dollar and ranked among the top crypto assets by market capitalization as of June 16, 2023.

- USDT (Tether)

- USDC (USD Coin)

- BUSD (Binance USD)

Legal tender-backed stable coins are linked to the value of legal tender because the issuer holds sufficient backing assets and is recognized as having equivalent value to legal tender.

For the three stable coins listed as representative examples, the issuer can exchange them 1:1 for U.S. dollars by following a procedure specified by the issuer, and providing a redemption mechanism is the basis for price stability.

In conjunction with this, the ability to ensure that redemptions can be carried out is also an important consideration. Unless the issuer can be sure that it has assets equal to or greater than the amount of stave coins issued, it cannot be trusted to be able to carry out redemptions for all holders.

Against this backdrop, many issuers regularly publish reports on their underlying assets. Issuers generate income by investing a portion of their assets in low credit risk assets such as government bonds, while collateralizing the assets with cash equivalents.

Crypto asset-backed

As the name implies, crypto-asset-backed stablecoins are stablecoins whose value is backed by crypto-assets.

Typical crypto-asset-backed stablecoins include

- DAI

- sUSD

When crypto assets are used as collateral, a collateral ratio equal to the amount of issuance is not sufficient. This is because, unlike legal tender, crypto assets are highly volatile (price fluctuations are large), and there is a risk of a collateral breakdown if the price of the crypto asset declines.

For this reason, crypto-asset-backed stave coins often introduce “overcollateralization” so that they can retain value even if the price of the crypto-asset they are collateralizing falls; in the case of DAI, the on-chain data shows that as of June 16, 2023, it is over 160% collateralized.

In the case of DAIs, if the crypto assets pledged as collateral fall below the minimum collateral ratio, they must either invest additional collateral funds or accept forced settlement.

Crypto-asset-backed stablecoins are considered to be less capital efficient due to the need for excess collateral, but they function as stablecoins that are complete in the crypto world.

Algorithm type (unsecured)

Algorithmic (unsecured) stable coins have no assets backing them and their value is held constant by an algorithm.

Typical algorithmic stablecoins include

- FRAX

- TerraUSD (UST)

- Magic Internet Money (MIM)

Although there are a variety of algorithmic stablecoins with different mechanisms in the crypto asset market, they all share the same goal of trying to keep prices constant by controlling market supply and demand.

For example, consider an algorithmic stablecoin that is linked to the US dollar. If an algorithm is employed that encourages “selling” when the market price is above $1 and encourages “buying” when the market price is below $1, it should theoretically function as a dollar-linked stablecoin.

In the case of USTs, this mechanism is achieved using governance tokens, whereby one UST can be exchanged at any time for a dollar’s worth of governance token LUNA, thereby creating an arbitrage incentive and stabilizing the value to a dollar.

commodity type

Commodity-type coins are stable coins whose value is backed by physical assets (commodities) such as gold and oil.

While physical assets have value in their own right, they also have the disadvantage of being difficult to transport and divide. Commodity-type stable coins are characterized by the fact that they have the same value as physical assets, can be easily traded, and can be purchased in small amounts, complementing the disadvantages of physical assets.

The mechanism is similar to that of a legal tender-backed security. The issuer holds a physical asset (commodity) as collateral, and the perceived equivalence to the physical asset is the basis for the price linkage.

Paxos Gold (PAXG) and Zipangu Coin (ZPG) are well-known examples of commodity-type stable coins.

Stable coin depegging case study

As explained so far, stablecoins have rapidly expanded their market size over the past few years. However, the need for regulation has recently been discussed around the world.

This is due to the questionable stability of stablecoins. While some stablecoins maintain their value stably over the long term, others have inadequate price maintenance mechanisms, and in some cases, the value of stablecoins has collapsed.

Here is a case study of an actual depegging (deviation in value) of a stablecoin.

Collapse of UST

One of the most talked-about cases of depegging to date is the collapse of the UST in 2022.

UST is an algorithmic stablecoin and employs a mechanism to stabilize its value by adjusting the supply of governor tokens, LUNA and UST. Just prior to the collapse, LUNA and UST were both large enough projects to rank among the top 10 crypto assets in terms of market capitalization.

On May 10, 2022, the value of USTs fell to $0.60 in a significant de-peg triggered by large volume sales of USTs. Although the value temporarily recovered to around $0.95, the simultaneous selling of LUNA and USTs due to the spread of credit concerns was unstoppable, and both LUNA and USTs eventually collapsed.

The Anchor Protocol, a lending protocol of the Terra Network, allowed USTs to earn a high interest rate of approximately 20% APY when deposited. Therefore, the amount of USTs circulating in the market was small, and the price of USTs tended to collapse.

Another factor was inadequate reserves held by the operator: Terraform Labs, the operator of Terra, had $3.5 billion worth of BTC in a fund in case the peg was removed. However, the market capitalization of LUNA and UST just prior to the crash (May 7, 2022) was $23.3 billion and $18.7 billion, respectively, far larger than the reserves and insufficient to absorb the sell-off due to credit concerns.

Algorithmic stablecoins have no underlying assets, so even before the crash, there were voices pointing out the risks involved. However, the fact that cryptocurrency with a market capitalization of over 6600 million dollar became nearly worthless in a matter of days highlights the risk of algorithmic stablecoins once again.

Price fluctuations occur even with collateralized stave coins.

So, it is not the case that a divestment will not occur if the coin is a backed stable coin.

When the UST collapsed, credit concerns spread not only to algorithmic coins but also to stablecoins as a whole, with the legal tender-backed USDT following the UST’s decline and pegging the price to $0.95 at one point.

In 2020, crypto asset-backed DAIs also experienced a de-pegging; when the cryptocurrency market crashed in March 2020, MakerDAO’s auction system failed to function properly, resulting in a $4 million liability. To resolve the collateral shortage, Maker DAO decided to issue additional governor’s tokens MKR, but since auction bids had to be made in DAI, the price of DAI temporarily soared to $1.12 due to increased demand for DAI.

Due to the nature of stablecoin, which is freely traded on the open market, deviations from the base price may occur depending on supply and demand conditions. However, when backed by assets, even if a deviation occurs, there is an incentive to buy and sell against the price to eliminate the deviation, and the peg can be recovered.

On the other hand, since there is no collateral for algorithmic stablecoins, the price maintenance mechanism is left solely to the algorithm. The author believes that the use case for algorithmic stablecoins will not expand unless a mechanism is developed to maintain the peg even in extreme trading events such as a run on the market.

Regulation of stable coins

While the convenience of stablecoins has been recognized, the need for appropriate regulation has been discussed, as some stablecoins are not stable in value.

Because stablecoins are cryptographic assets issued on the blockchain, P2P money transfers are possible. While this characteristic is convenient, it also poses the risk of being used for money laundering or terrorist financing purposes, since money can be transferred anywhere in the world.

Against this background, the need for regulation is being discussed, but since it is difficult to address P2P remittances through regulations in a single country, apart from establishing regulations in a country or region, regulations at the international level should also be considered.

Regarding the international regulatory framework for stable coins, an organization called the FSB or FATF is currently leading the regulation of stable coins.

FSB, which stands for Financial Stability Board, is an international organization responsible for measures, regulation, and supervision related to international financial stability. Representatives of central banks and other multi-financial organizations from 25 major countries and regions participate in the FSB.

In October 2022, the FSB published a document on “International Regulation of Crypto Asset Related Activities”. The document states that for global stablecoins, high regulatory standards should be applied with respect to user redemption rights and requirements for value stabilization mechanisms.

The FATF, which stands for Financial Action Task Force, is a partnership of major countries that creates standards to prevent money laundering and the financing of terrorism.

In July 2020, the FATF published the FATF Report to G20 Finance Ministers and Central Bank Governors on so-called stablecoins. The document points out that P2P transactions via unhosted wallets pose a risk of money laundering and terrorist financing, and that effective regulation is needed.

National and regional units are considering various methods of regulation. For example, the EU passed the Crypto Asset Market Regulation Bill (MiCA) in October 2022, which includes such provisions as allowing issuers of stable coins to allow holders to exchange them for the underlying asset at any time.

Comments